Management Buyouts & Liquidation in Startup Funding: Ownership, Exit, and Endgames

Equity, Exits, and Hard Calls: The Truth About Buyouts and Liquidation

Startup funding isn’t just about raising capital—it’s also about long-term strategy, ownership dynamics, and preparing for eventual exit scenarios. While much of the spotlight is on IPOs and high-profile acquisitions, Management Buyouts (MBOs) and Liquidation Scenarios represent two critical, often under-discussed outcomes in the startup lifecycle. These events may signal dramatic shifts in control, reflect a change in business direction, or, in some cases, mark the end of a startup’s journey.

In this blog, we’ll unpack the strategic role of MBOs—where internal teams buy out external stakeholders to regain ownership—and explore what happens when startups face liquidation, voluntarily or otherwise. You’ll learn why these scenarios arise, how they’re structured, what they mean for founders, investors, and employees, and how to navigate them with foresight rather than fear. Whether you’re aiming to reclaim control or preparing for a worst-case wind-down, understanding these exit strategies is essential for smart, holistic startup leadership.

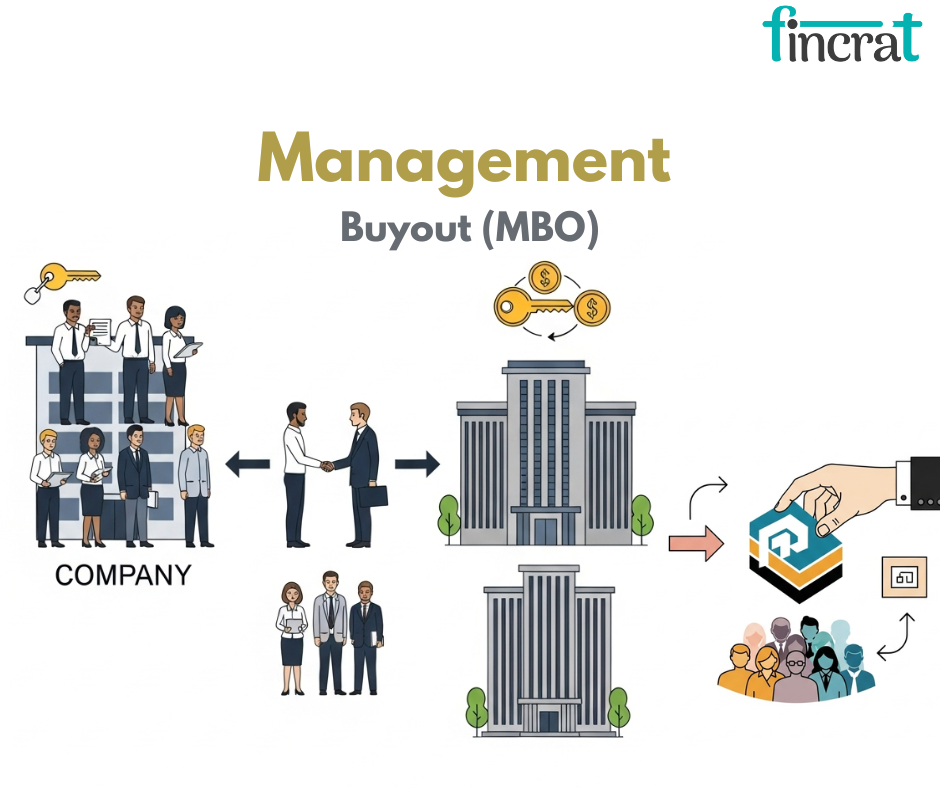

What Is a Management Buyout (MBO)?

- A Management Buyout (MBO) is a financial deal whereby an existing company management purchases ownership of the company they are currently operating.

- This can be either full or partial and is usually funded using a combination of personal resources, private equity, and debt (leveraged financing).

- The objective is to shift control from current shareholders—usually founders, private investors, or parent companies—to managers who already know the business and operations.

- In an MBO, the management group—typically the CEO, CFO, or senior management—is convinced of the long-term prospects of the business and wishes to acquire ownership so that they can steer it into the future.

- Existing owners might be seeking to exit for reasons of retirement, strategic changes, or disposal, and selling to internal management maintains continuity of operations and usually leads to an easier transition.

- In contrast to external takeovers, MBOs are insiders who already have knowledge of the company's problem areas, culture, and prospects for growth, minimizing due diligence time and risk of execution.

- By Investopedia, management buyouts account for around 20–25% of total private equity buyouts each year in the U.S. and Europe.

- MBOs are more prevalent in profitable, stable, cash-generating businesses, especially in the mid-market range.

- Private equity firms often finance more than 50%-60% of MBO transactions, investing capital for equity and long-term returns.

- MBOs can take the form of leveraged buyouts (LBOs), with debt being taken over secured against assets and cash flows of the firm.

- Management groups tend to be given more freedom and remuneration after the buyout, while taking on higher financial risk.

Why Do Management Buyouts Happen?

MBOs happen for a variety of strategic, financial, and operational reasons. Here are the most common scenarios:

- Owner Exit or Retirement: When a founder or major shareholder wants to step away from the business, selling to the management team can ensure continuity and preserve company culture.

- Strategic Realignment: In larger corporations, a business unit may be sold to its managers if it's no longer core to the parent company's strategy.

- Belief in Growth Potential: Management teams may feel they can increase the company's value significantly if they have ownership and full decision-making authority.

- Private Equity Support: PE firms often back MBOs by providing capital to management teams with a strong growth plan.

Key Characteristics of an MBO

MBOs are unique compared to external acquisitions. Here’s what sets them apart:

- Led by insiders: The buying party is the current management team, not an outside buyer.

- Continuity: Operations remain largely unchanged, which minimizes disruption to employees, customers, and suppliers.

- Financing: Often funded through loans, seller financing, or private equity—sometimes as a leveraged buyout (LBO) using the company’s assets as collateral.

- Common in succession planning: Particularly when founders retire or when a corporate parent divests a division.

How Are MBOs Funded? (Breakdown of Capital Sources)

Management Buyouts (MBOs) typically require significant capital, as the management team needs to purchase a controlling or substantial stake in the company.

Since most management teams don’t have the personal resources to fund the buyout on their own, MBOs are usually financed through a combination of funding sources.

Here’s a breakdown of the most common methods used:

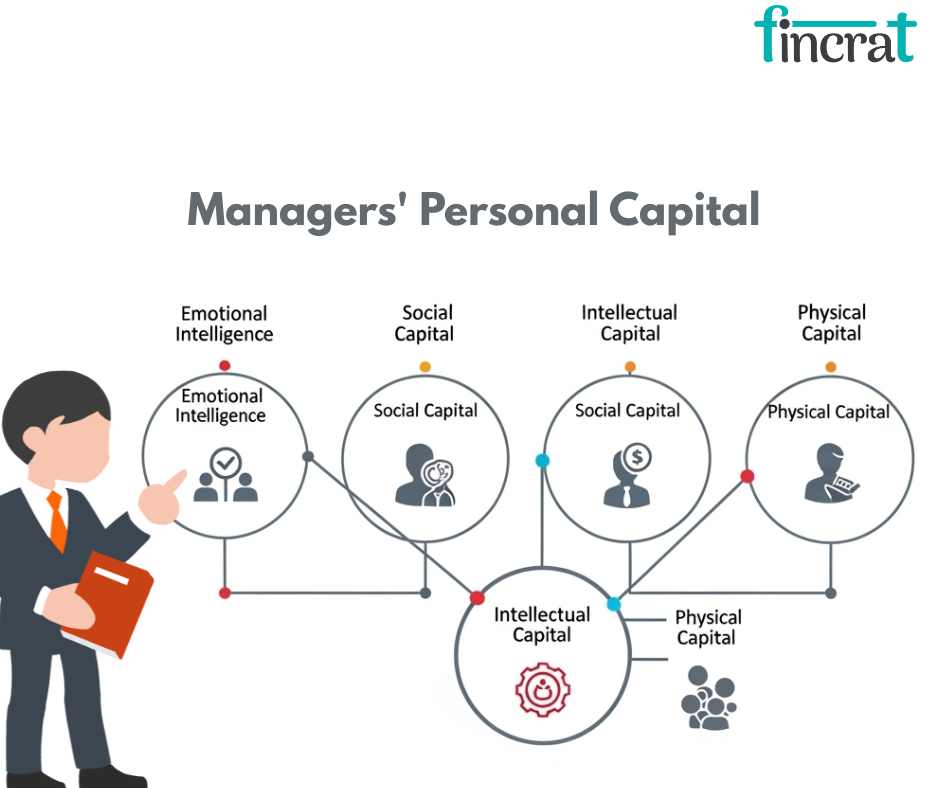

1. Managers' Personal Capital

- Managers can invest a fraction of their own funds or personal capital to show commitment and bear some of the risk.

- Though this fraction is typically small, it's crucial for winning the trust of other financing stakeholders.

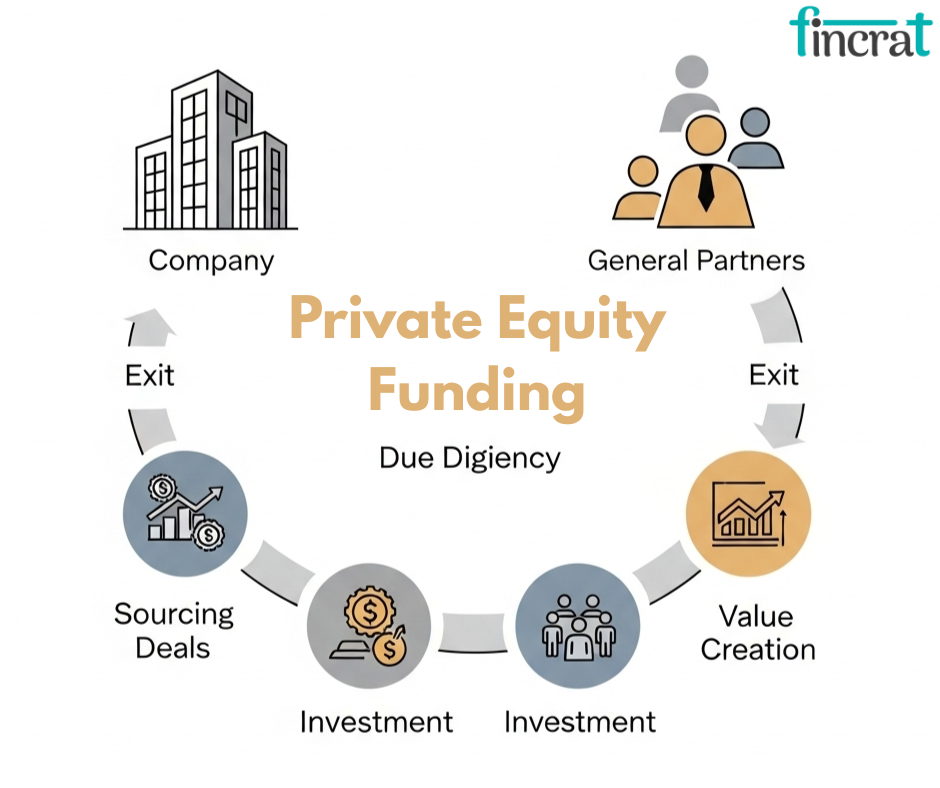

2. Private Equity Funding

- Private equity (PE) companies are among the most frequent financiers of MBOs.

- They invest money in return for business equity and typically include strategic guidance and operating expertise.

- PE firms like profitable, cash-flow positive businesses.

- They usually retain ownership for 4–7 years before exiting.

- PE financing can include board participation or performance milestones.

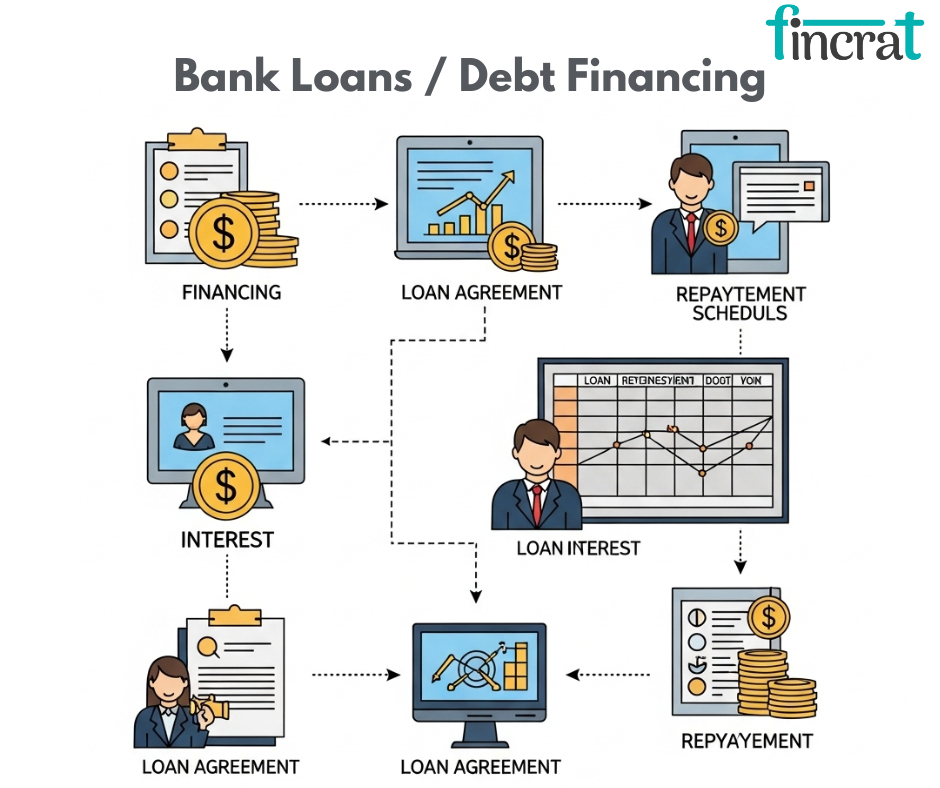

3. Bank Loans / Debt Financing

- MBOs typically include leveraged buyouts (LBOs), where a loan is borrowed against the assets and future profits of the business.

- This introduces financial risk but enables the team to own the business with less initial capital.

- Comprises term loans, mezzanine financing, or asset-backed lending.

- Typically needs good cash flow and minimal existing debt.

- High leverage puts a lot of financial pressure after the buyout.

4. Seller Financing

- At times, the existing owner is willing to accept a portion of the payment in installments, in effect providing a loan to the management team.

- It minimizes the amount of upfront cash required and may be more favorable in terms than outside financing.

- Applicable in family businesses or small businesses.

- Keeps the seller interested in the success of the transition.

5. Earn-Outs and Deferred Payments

- Management can negotiate a deal in which some of the purchase price is paid contingent on future performance, limiting upfront funding requirements while incentivizing future success.

6. Equity Rollovers

- In a number of MBOs, the incumbent owner can maintain a minority equity stake, under which they can roll over equity in the new company.

- This helps in limiting the cash requirement and indicates continued confidence in the business.

Risks & Rewards of Management Buyouts

Pros:

- Autonomy and control for managers

- Financial upside if company grows

- Strategic alignment between ownership and operations

- Continuity for staff and customers

Cons:

- High financial risk for managers

- Debt burden can limit future flexibility

- Pressure from private equity performance targets

- Potential conflicts of interest during negotiation

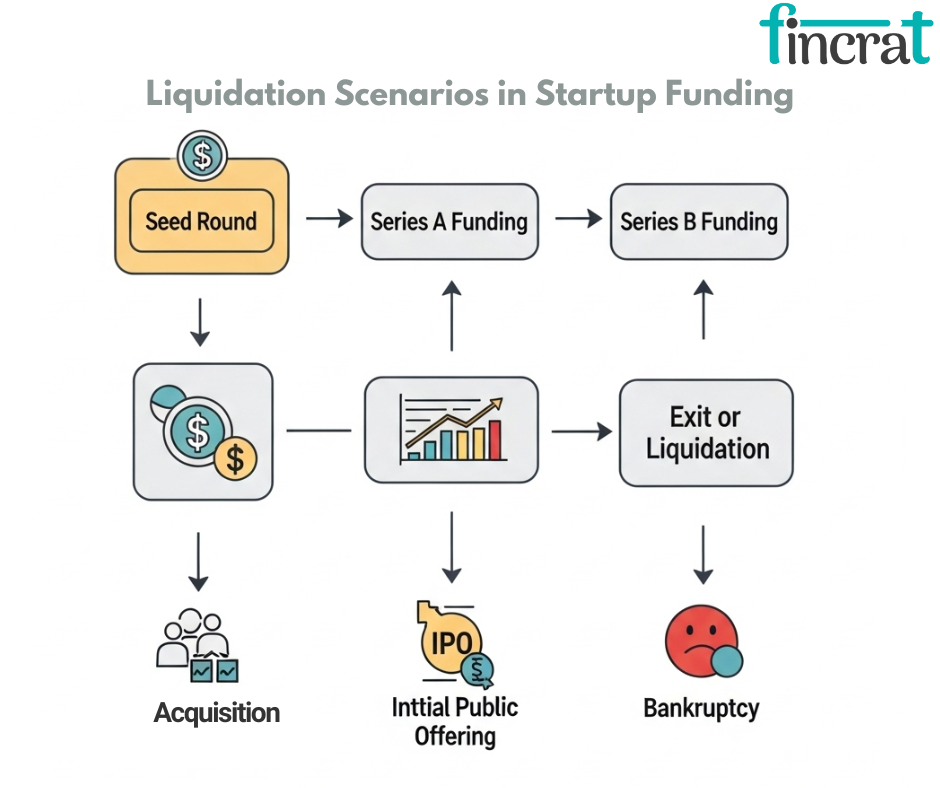

Liquidation Scenarios in Startup Funding

- Liquidation scenarios describe the potential situations where assets of a startup are being sold to settle debt and return any excess value to shareholders.

- These are typically when a firm is unable to become profitable, raise additional capital, or obtain an acquisition or IPO.

- Liquidation is generally considered a last resort, yet it's an important part of the startup funding cycle that affects investors, founders, and employees.

- Over 80%- 90% of startups go out of business, and liquidation is the most prevalent outcome.

- According to CB Insights, 38%- 40% of startups collapse because of insufficient capital or fundraising failure, usually resulting in coerced wind-downs or liquidations.

- In the majority of liquidations, common shareholders (employees with stock options included) receive minimum or no reward.

5 Common Liquidation Scenarios Explained

1. Voluntary Liquidation

- In this case, the founders or the board deliberately decide to wind up the company—typically because it is no longer sustainable, has run out of money, or the market opportunity has evaporated.

- Assets are disposed of in order to settle debts.

- The remaining proceeds are distributed to preferred and common shareholders (in priority).

- Typically occurs when the firm has some assets but no legal compulsion.

2. Involuntary Liquidation (Bankruptcy)

- This occurs when creditors or courts compel the company to liquidate because of unpaid debt. It's regulated by bankruptcy laws and usually ends in complete loss for equity owners.

- Creditors are paid first, then preferred stockholders (if anything is left).

- Common stockholders typically receive nothing in these situations.

- Can include restructuring if the company files Chapter 11 bankruptcy (in the U.S.).

3. Acquihire with Liquidation Terms

- Sometimes, a struggling startup is "acquihired" (purchased for its people) by a larger firm.

- The buyer company buys the people but not the product, and liquidation takes place to legally shut down the original company.

- Shareholders might get little or no returns.

- Members of the team are usually given new positions as part of the agreement.

- Debts might be paid off prior to the deal.

4. Asset Sale (Fire Sale)

- A distressed startup can sell its tangible and intangible assets (tech, IP, inventory) to another firm.

- Typically returns only to debt holders and preferred investors.

- Familiar with early-stage shutdowns.

- May be insufficient to cover full debt obligations.

- Often quick and at discounted prices.

5. Wind Down with Investor Preference Enforcement

- As a firm winds down, liquidation preferences (described in the term sheet or shareholders' agreement) become activated.

- Preferred shareholders can recover 1x–2x their investment prior to common shareholders' receipt of any distribution.

- Seniors with liquidation rights are given priority.

- ESOP holders and founders tend to receive nothing if the result is below liquidation preference levels.

Secondary Sales vs. Primary Rounds vs. IPO vs. Management Buyouts vs. Liquidation

- In startup funding, not all capital events serve the same purpose—or carry the same implications.

- Primary rounds involve selling new shares to bring fresh capital into the business, helping fund growth and operations.

- In contrast, secondary sales allow existing shareholders—like early employees or investors—to sell their shares to new investors, providing liquidity without diluting the company.

- An IPO (Initial Public Offering) takes things a step further, listing the company on a public exchange, unlocking massive liquidity and visibility, but also bringing regulatory scrutiny and loss of private control.

- Management buyouts (MBOs) represent a different kind of shift—where internal stakeholders, such as founders or executives, purchase control back from external investors, often using debt or external financing, aiming to take the company private or reorient strategy.

- Finally, liquidation occurs when a startup winds down, typically due to unsustainable operations or a failed pivot. Assets are sold off to pay debts and investors, often leaving minimal returns.

- While liquidation signals the end, MBOs, IPOs, and secondaries are all tools for restructuring or scaling ownership and liquidity—each with vastly different outcomes for the team, investors, and the future of the company.

Final Take: Why Ownership, Liquidity, and Exit Paths Define Your Startup’s Trajectory

In the startup journey, how you raise, share, and exit equity isn’t just financial housekeeping—it’s strategic leadership. Understanding the nuances between secondary sales, primary rounds, IPOs, MBOs, and liquidation gives founders the power to make informed, future-proof decisions.

Whether you're unlocking liquidity without giving up control, preparing for an investor-backed growth sprint, or navigating your company through a critical ownership transition, these mechanisms shape your long-term outcomes.

In the end, smart capitalization isn’t about chasing headlines—it’s about building value, rewarding the right people, and sustaining momentum through every chapter of the startup lifecycle.Own the equity. Master the exits. That’s how real startup leadership works.

"Equity isn’t just ownership—it’s leverage, loyalty, and your legacy."