Startup Valuation Demystified: What Every Founder Needs to Know Before Raising Capital

Know your worth, understand the methods, and learn how to negotiate startup valuation like a seasoned founder

Valuing a startup isn’t just a numbers game—it’s the art and science of balancing vision, traction, market potential, risk, and team execution. Whether you’re raising a pre-seed round or preparing for Series B, your startup’s valuation determines how much capital you can raise—and how much of your company you’ll give up in return.

This comprehensive guide breaks down everything founders need to know about startup valuation: key concepts, proven methods, influencing factors, and how to negotiate valuation without losing control.

What Is Startup Valuation ?

- Valuation of a startup refers to the method of ascertaining the present value of a startup business.

- Unlike mature companies with consistent revenues, startups tend to be valued according to their potential, rather than their past financial performance.

- The valuation indicates the amount of money that investors are willing to spend on an ownership share and assist in establishing the proportion of the company that they get in return for investment.

- Startup valuation is crucial during fundraising because it directly impacts equity distribution, investor negotiations, and the company’s ability to attract capital.

- It considers factors such as the founding team’s expertise, product potential, market opportunity, competitive landscape, traction, revenue forecasts, and even external market conditions.

- In the earlier phases, when startups might not have profits or even revenues, approaches such as the Berkus Method, Scorecard Method, or VC Method come into the picture rather than standard financial measures.

- As startups mature, increasingly data-driven approaches like Discounted Cash Flow (DCF) or Comparable Company Analysis enter the scene.

- Early-stage startup valuations in 2024 ranged from $3 million to $15 million, depending on location, industry, and traction, according to AngelList.

Why Startup Valuation Matters – More Than You Think

Startup valuation isn't merely assigning a price to your company—it determines your leverage, your future, and your trajectory of growth.

Here's why it's important:

- Equity and Ownership:The more valuable you are, the less equity you sacrifice for the same level of capital. It determines straightaway how much of your business you get to hold on to as a founder.

- Investor Perception:An accurate valuation generates investor confidence. Too high, and you scare off investors. Too low, and you send a message of lack of confidence or unfamiliarity with your market.

- Funding Roadmap:Your valuation provides the template for subsequent rounds. An ill-calculated early valuation can lead to a "down round" later—a warning sign for subsequent investors.

- Negotiation Power:Valuation impacts everything in the term sheet—from control of the board to liquidation preferences. Do it well, and you negotiate from strength.

- Team Incentives:Stock options for employees are valuation-dependent. A savvy valuation allows you to get great talent and keep great talent, while safeguarding the option pool.

Valuation is not a number. It is a strategic handle that drives your startup's trajectory, credibility, and final success in the perception of investors, acquirers, and the marketplace.

Pre-Money vs. Post-Money Valuation: Know the Difference

- Startup Valuation of a startup is particularly important at fundraising, particularly in deciding how much ownership an investor gets for their investment.

- Two basic terms in the process are pre-money valuation and post-money valuation.

- These terms establish the value of a startup at various stages of a deal and have a direct bearing on ownership percentages and negotiations between investors and founders.

- Pre-money valuation is the projected value of a startup prior to the addition of any new outside capital or investment.

- It is the value one assigns to the company from what it is today, consisting of assets, product development, team, intellectual property, traction, and growth potential.

- This valuation would normally be established using techniques like market comparables, investor intuition, or strategic consideration and is employed to anchor investment discussions.

- A pre-money valuation that is higher usually benefits founders since it enables them to sacrifice less equity for the same level of funding.

- Conversely, post-money valuation refers to the company's value following the new investment. It is obtained by adding the investment to pre-money valuation.

- For instance, if a startup is worth ₹10 crore prior to investment and is provided with ₹2 crore of funds, the post-money valuation is now ₹12 crore. This figure is a representation of the sum total of the worth of the startup plus the fresh capital added. It is most commonly utilized to ascertain the amount of ownership the investor shall have. In this scenario, the investor would have 16.67% ownership of the firm (₹2 crore / ₹12 crore).

- It is essential for founders and investors to understand the distinction between these two terms.

- Misunderstanding them may result in negative agreements, like conceding too much equity or overvaluing the business.

- Founders have a better chance of getting control by understanding pre-money and post-money valuation.

- This understanding enables founders to control the company, strategize the distribution of equity (particularly for subsequent rounds of fundraising), and establish trust with potential investors.

- As stated in PitchBook's report, startups that have a clear pre-money valuation and tailor term sheets accordingly have a 30% higher chance of getting better financing terms compared to those that do not.

Top 5 Startup Valuation Methods You Must Know

Valuation Method refers to the approach or framework used to determine the economic worth of a startup at a given point in time. These methods are crucial for both founders and investors to agree on how much a company is worth before fundraising, acquisitions, or exits.

- Berkus method

- Scorecard method

- DCF (Discounted Cash Flow)

- VC method

- Comparable companies method

Startup valuation isn’t a guessing game—it’s guided by structured methodologies. The right method depends on your stage, traction, and data availability.

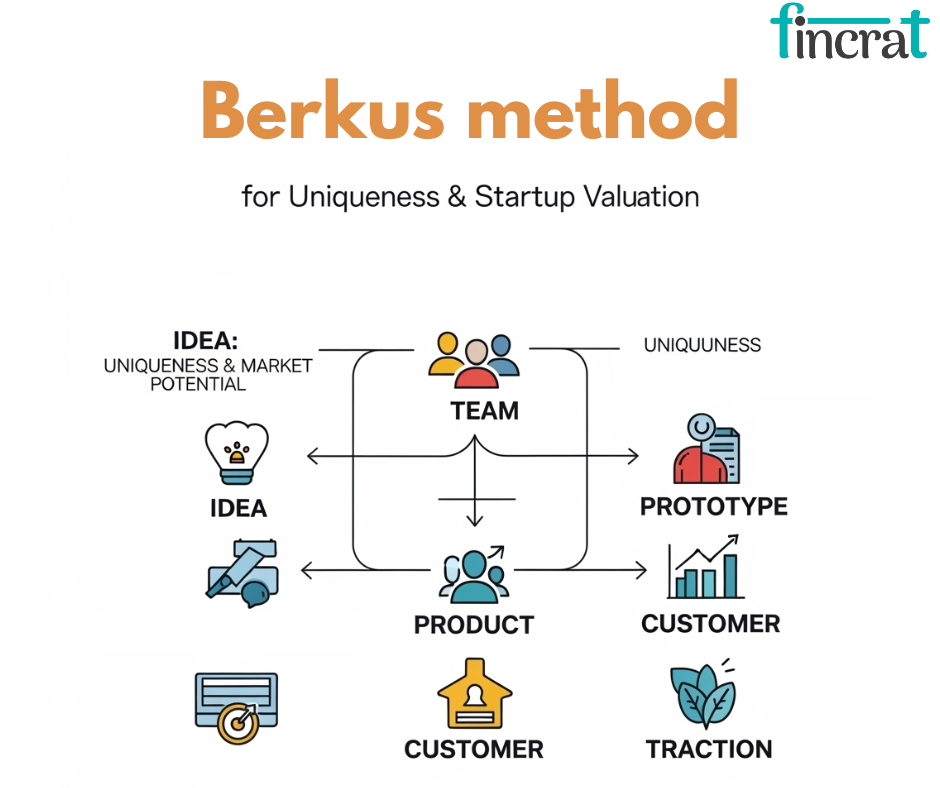

1. Berkus Method

- The Berkus Method is a method of valuing startups that can be used for early-stage ventures with no or minimal revenue.

- Developed by American angel investor Dave Berkus, this method gives financial value to five main success factors, each of which stands for a key area in the potential of the startup.

- The solidity of the idea,

- The product or prototype development,

- The quality and experience of the management team

- strategic partnerships and alliances,

- product launch or sales milestones.

- Either can be worth up to $500,000 (or equivalent in other currencies), with an overall limit of approximately $2 million to $2.5 million.

- This approach focuses on qualitative potential, not current finances, and is best suited for startups in the idea or prototype phase.

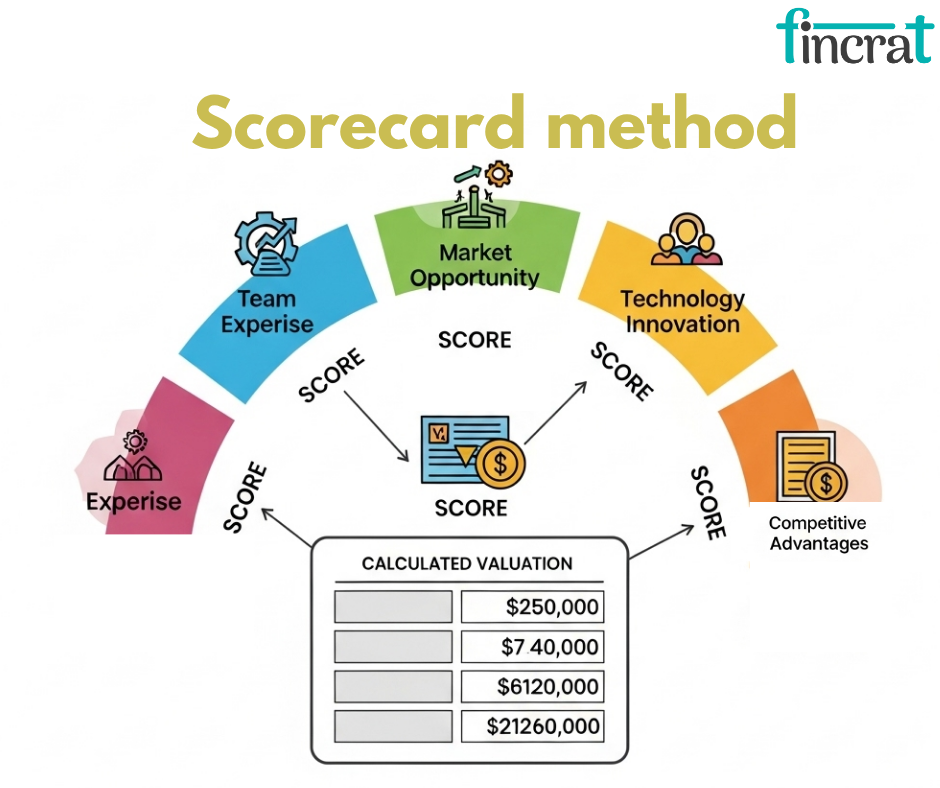

2. Scorecard Method

- Another widely used technique to estimate the value of early-stage startups is the Scorecard Method, or the Bill Payne Method.

- It compares the target startup with similar funded startups in the same sector and geographical area.

- A base average valuation is determined based on market information, and adjustments are then made based on a number of weighted factors: team strength, opportunity size, product or technology, competitive landscape, marketing/sales strategy, need for incremental investment, and other risk factors.

- Each of the factors is scored in terms of percentage over or under average, and this weighted score is then applied to the base valuation to arrive at the final estimate.

- The advantage of this method is that it combines qualitative considerations with the regional benchmarking of valuations.

- Angel groups frequently adopt this method, particularly in ecosystems such as India's Tier 1 cities and Silicon Valley, where comparable funding data is easily available.

3. DCF (Discounted Cash Flow) Method

- The Discounted Cash Flow (DCF) Method is a more financial and fact-based method, applicable to startups with some level of history of revenues or sound financial projections.

- It entails the projection of the startup's anticipated future cash flows and discounting it to the present value with a discount rate that takes into consideration the risk of the business.

- Since startups are risky in nature, higher discount rates (20–50%) are applied.

- This technique provides an intrinsic value on the basis of projected profitability and risk, and though potent, it demands realistic projections and robust financial assumptions.

- Based on PitchBook, startups that apply DCF with realistic cash flows and a discount rate of 30–50% tend to come up with valuations 30–40% below optimistic, unadjusted figures.

4. VC Method (Venture Capital Method)

- The Venture Capital Approach is applied by VC firms across the board to estimate startups' value based on anticipated exit situations.

- It begins by approximating the firm's value at exit (using anticipated earnings and industry exit multiples) and then solving backward to derive its current value.

- The approach takes into account the anticipated Return on Investment (ROI) that the VC seeks, and the time frame of the exit (usually 5–7 years).

- For instance:

- Pre-Money Valuation=Post-Money Valuation−Investment Amount

- The approach is very handy for later-stage startups whose growth metrics and exit situations are more certain.

5. Comparable Companies Method

- Comparable Companies Method, or "comps" technique, assesses a startup by referencing similar publicly listed companies or newly funded startups in the same industry or geographic location.

- Valuation multiples—like Price-to-Earnings (P/E), Price-to-Sales (P/S), or Enterprise Value-to-EBITDA—are utilized to compare the startup's potential value.

- For instance, if similar companies are worth 10× revenue and the startup's projected revenue is ₹5 crore, the valuation would be estimated at ₹50 crore.

- It presumes efficient markets and available data and tends to be employed when there are sufficient comparable benchmarks.

- It gives a market-oriented view but can be distorted by variations in business model, stage, or geography.

- 70%-80% of Series A and B transactions in 2024 were driven by similar multiples, tech and SaaS startups are typically valued at 8–12× revenue depending on growth rate, per CB Insights.

10 Key Factors That Influence Startup Valuation

Several qualitative and quantitative factors influence how a startup is valued, including:

1. Stage of the Startup

- The value of a startup heavily relies on its stage of development. Early-stage startups—those in the idea or MVP stage—have high uncertainty and sparse financial information, which results in lower valuations.

- As the startup ages, gains paying customers, and attains product-market fit, its risk profile lowers, which usually corresponds with a higher valuation.

- Advanced phases such as Series A or B usually witness considerably higher investor confidence, with room for better funding terms and larger amounts of capital inflow.

- A startup with only an idea will be worth ₹2–3 Cr, whereas the same startup with consistent monthly revenue (MRR) can command a valuation of ₹10–15 Cr

2. Market Size and Opportunity

- Investors examine closely the size and growth opportunity of the market a startup is entering.

- A bigger Total Addressable Market (TAM) means there is more potential for revenue growth, scale, and returns.

- Startups in billion-dollar markets or upstart industries typically command higher valuations because they imply long-term scalability and profitability.

- The larger the problem being solved—and the larger population of people who require the solution—the more valuable the company seems.

- Startups with a TAM of over $1B command more VCs' attention, growing valuation by 30–40%, PitchBook reports.

3. Traction and Revenue

- On-ground traction proves product validity and customer demand. All the following metrics imply higher perceived value: monthly active users, recurring revenue, user engagement, low churn.

- A startup with increasing revenue, good retention, and good unit economics conveys lower risk and higher potential for returns.

- Even pre-revenue startups can increase valuation if they demonstrate strong user adoption, waiting lists, or solid pilot programs.

- Startups demonstrating >10% MoM growth or ₹1 Cr+ ARR tend to receive 2–3× higher valuations than comparable early-stage startups, albeit with no traction.

4. Strength and Experience of the Team

- Investors tend to prefer the quality of the founding team over the idea.

- A team with established experience, particularly in the same domain, tends to increase a startup's valuation drastically.

- Repeat founders who have previously founded or exited startups get more valuations because they're perceived as being able to perform under stress, assemble strong teams, and handle scaling issues.

- Complementary and diverse sets of skills within the team are also valuable assets.

- YC-backed startups with repeat founders close 25%–40% more capital and get higher valuations on average.

5. Product and Technology Differentiation

- Startups with novel technology, intellectual property, or defensible product moats command higher valuations.

- When the product is difficult to copy or holds a distinctive superiority over current offerings, investors view it as a moat—insulating long-term value and market leadership.

- This is particularly significant in industries such as AI, deep tech, or biotech, where innovation has a direct influence on valuation multiples.

- Deep-tech startups or AI-powered SaaS platforms tend to have valuation multiples of 8–12× revenue, while plain vanilla tech platforms fetch only 3–5× revenue.

6. Business Model and Scalability

- Asset-light and scalable business models—particularly those with recurring revenues such as SaaS—are more highly valued as they offer growth at a faster rate with lower costs.

- Startups that can provide services to more customers without proportionally raising expenses attract investors.

- Recurring revenue streams, such as subscription, enhance valuation by limiting risk and providing more insight into future cash flows.

- SaaS firms have higher valuation multiples because of recurring income, usually between 10–20× ARR at growth stages.

7. Financial Metrics

- Startups with solid fundamentals—low burn rate, high gross margins, high customer lifetime value (LTV), and optimized customer acquisition cost (CAC)—are viewed as more sustainable and valuable.

- These figures indicate a startup's ability to control its finances and whether it can grow effectively.

- A high LTV:CAC and fast CAC payback can especially be convincing for investors.

8. Competitive Landscape

- If a startup is in a very saturated or commoditized space, its valuation can be lower unless it has strong competitive differentiation.

- A clear value proposition, distinct brand, or network effects may assist the company in standing out.

- Whether they can protect market share and maintain growth against copycats or incumbents impacts how investors view valuation.

- A ratio of LTV:CAC >3:1 is regarded as healthy and enhances investor confidence and valuation.

9. Macroeconomic Conditions

- Wider economic trends, including interest rates, inflation, geopolitical stability, and the terms of capital markets, have a major impact on startup valuations.

- In bull markets or times of high investor confidence, valuations increase across the board.

- Conversely, economic downturns or funding stops can trigger steep valuation corrections, even for successful startups.

- Global startup valuations declined 20–30% in the tech slump as a result of increased interest rates and investor conservatism.

10. Investor Sentiment and Industry Trends

- Investor trends can dramatically influence the valuation of startups.

- During a particular year, industries such as AI, climate tech, or fintech might be receiving top dollar valuations for hype, government subsidies, or newer success stories.

- Startups that fall into these popular sectors tend to raise more funds at higher valuations merely due to higher demand and competition among investors.

- AI startups in 2024 raised 2–5× more than similar-stage traditional SaaS startups.

- 42%-50% of startups fail because there's no market need for their product or service, as stated by CB Insights—leaving market potential as one of the most significant valuation drivers.

How to Negotiate a Fair Valuation Without Losing Control

Negotiating a startup’s valuation is one of the most critical—and delicate—conversations between founders and investors. It’s not just about arriving at a number; it’s about aligning expectations, balancing equity dilution, and setting the stage for future funding rounds.

1. Know Your Numbers

- Founders should be familiar with their numbers before approaching any negotiation: revenue (or traction), burn rate, CAC, LTV, gross margins, market size, and competitor benchmarks.

- These numbers will form the basis of your valuation justification. Investors will examine them to estimate risk and growth potential.

- Ensure that your numbers are realistic, defendable, and attached to explicit growth expectations.

2. Understand Investor Psychology

- Investors are not only investing in a product—they're investing in your vision and your team's capability to bring it to fruition.

- They expect a good return on investment (ROI) in 5–10 years.

- Their valuation mindset will consider risk, industry trends, exit opportunities, and their required equity stake.

- Knowing what motivates them enables you to present stronger counterarguments during negotiations.

3. Strive For Fair, Not Exaggerated Valuation

- It's easy to try for the most valuation you can get, but overvaluation can come back to haunt you.

- An overvalued price in the early stages builds pressure to achieve aggressive targets and could make later fundraising more difficult if those numbers aren't reached.

- A reasonable valuation—on the basis of traction, team quality, and market potential—can enable you to establish long-term investor credibility and get more favorable follow-on rounds.

4. Awareness of Dilution

- Founders should know how much equity they are sacrificing.

- Normal early-stage transactions experience 10–25% dilution.

- Donating too much can leave founders under-motivated; too little can deter investor participation.

- Cap table planning and scenario modeling (e.g., on Google Sheets or cap table software) are necessary to see how it affects later rounds of funding.

5. Apply Benchmarks and Similar Deals

- Consider what comparable startups in your business, geography, and stage are worth. Websites such as PitchBook, Crunchbase, AngelList, or startup accelerators tend to give valuation standards.

- Showing comparable valuations makes your case more robust and anchors your Ask to actual market realities.

6. Use Multiple Offers (where you can)

- The best negotiation tactic is having options.

- If there are multiple investors in the running, you have leverage to negotiate improved terms.

- But never sacrifice diligence for speed—hurrying to close without due diligence on investors or excessive leverage usage can produce suboptimal long-term fit.

7. Be Attentive to Terms, Not Merely Valuation

- Valuation is only one aspect of the deal. Other term sheet components—such as liquidation preferences, board governance, ESOP pools, or anti-dilution provisions—can have material implications on founder equity and control.

- A slightly lower valuation with terms that are founder-friendly could be better than a high-valuation deal with unfavorable terms.

8. Don't Be Afraid to Walk Away

- If the deal devalues your business or contains aggressive investor rights, it's alright to say no.

- Not all capital is good capital.

- Founders should be discerning and long-term oriented in whom they bring on board.

Final Thought: Valuation Is a Conversation, Not a Conclusion

Valuation isn't a fixed number etched in stone—it's a dynamic, evolving conversation between founders and investors. It reflects not just what your startup is worth today, but what it could become tomorrow.

Factors like market sentiment, competitive landscape, investor appetite, and your ability to articulate a compelling vision all play a role.

Instead of obsessing over getting the “perfect” valuation, focus on creating alignment around your growth story, risk-reward balance, and mutual goals.

The real win isn’t just a high number—it’s securing smart capital on terms that empower long-term success.

“Investors don’t just buy equity—they buy belief , that’s what valuation reflects.”