Secondary Sales in Startup Funding: Unlocking Liquidity Without Losing Control

How Late-Stage Stakeholders Can Cash Out — Without Slowing the Startup Down

In the high-stakes world of startups, equity is often the only currency early founders, employees, and investors receive for their risk, sweat, and loyalty. But what happens when the company is soaring — yet no IPO or acquisition is in sight?

That’s where secondary sales come in — a growing trend among startups and investors seeking liquidity without issuing new shares or raising additional capital. Whether you’re a founder who’s spent 8 years building your company, an early employee holding vested stock, or an investor looking to rotate capital, secondary sales let you realize value today while the company continues to scale.

Let’s explore what secondary sales are, why they matter, who benefits, and how to execute them strategically.

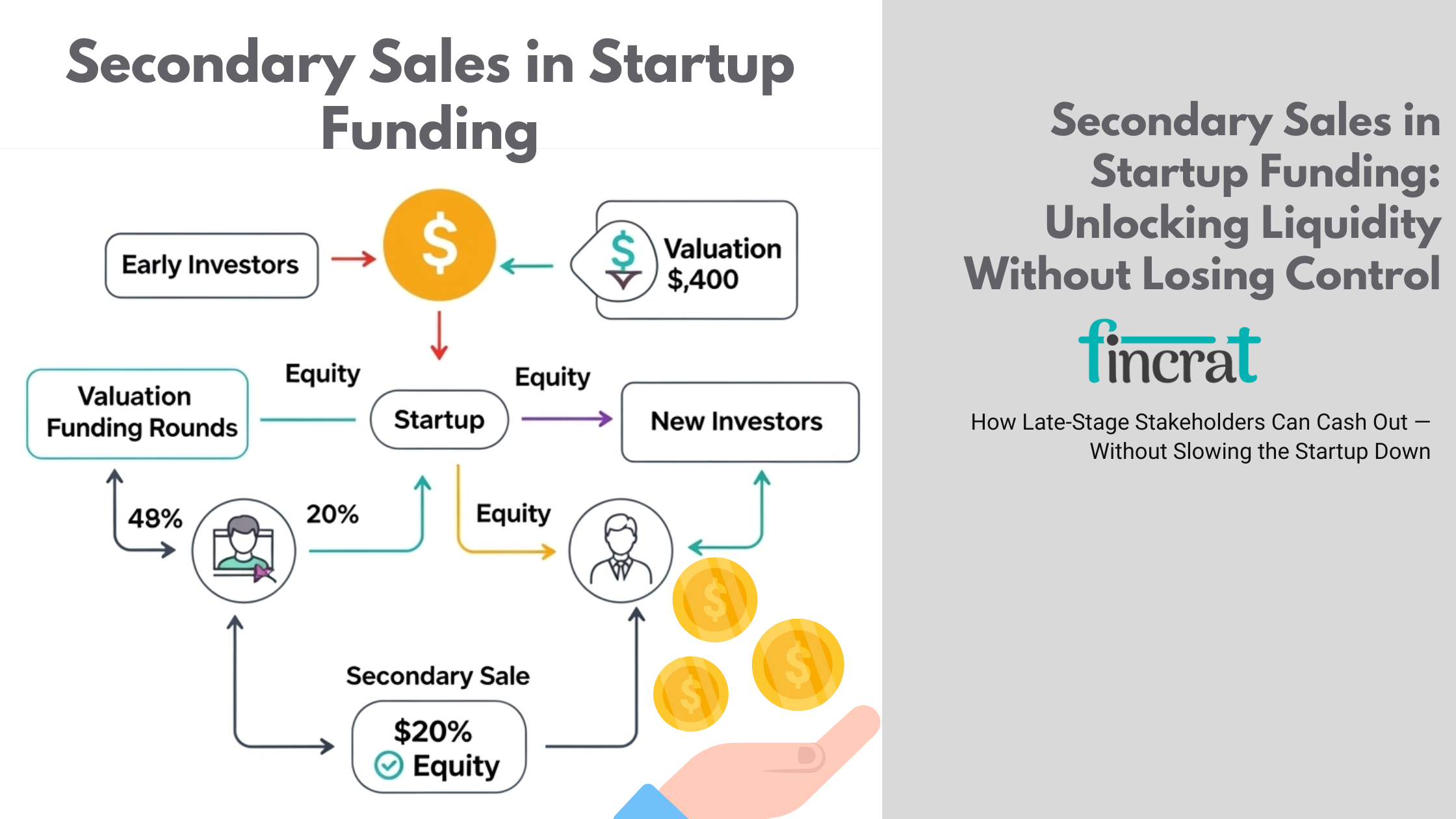

What Are Secondary Sales in Startup Funding?

- Secondary sales in startup financing are the sale of existing shares by existing shareholders—e.g., founders, employees, or early investors—to new shareholders or investors.

- Unlike a primary round of funding, where a firm issues fresh shares and raises new capital, secondary sales involve no fresh money flowing into the firm.

- The proceeds of the sale go straight to the selling shareholder.

- These sales are typical in late-stage startups (usually Series B or later), particularly those nearing exit events such as IPOs or acquisitions, or where the startup has passed major valuation milestones.

- More than 60%-75% of unicorn startups have enabled at least one secondary share sale round prior to IPO or acquisition.

- The global secondary private market size reached more than $100 billion in 2022, illustrating rising private equity liquidity demand.

- The time between a startup IPOing is now more than 10 years, and thus secondary sales are a key choice for early liquidity.

- Employees and founders will sometimes sell a small portion of their ownership to realize liquidity but also hold on to it for the long term.

- Secondary sales don't dilute existing shareholders, in contrast to primary equity rounds.

Why Secondary Sales Matter in Startup Funding

Here are the key points with descriptions:

- Enables Early Liquidity for Founders & Employees: Secondary sales allow founders, early employees, or executives to sell a portion of their equity and gain financial flexibility before an IPO or acquisition, often helping retain key talent.

- Helps Early Investors Realize Returns: Angel investors or early-stage VCs can partially or fully exit, freeing up capital for new investments and demonstrating a real return on their portfolio.

- Attracts Late-Stage Investors: Secondary opportunities can entice growth-stage investors who want equity without dilution or waiting for a primary round, making it easier to close larger deals.

- Does Not Dilute the Cap Table: Since no new shares are issued, the ownership percentage of existing shareholders remains unchanged, preserving equity for future fundraising rounds.

- Acts as a Confidence Signal: When top-tier investors buy secondary shares, it can signal belief in the startup’s long-term success—boosting credibility with the market and other stakeholders.

- Helps with Founder Retention: Monetizing some equity reduces pressure to exit prematurely, allowing founders to focus on long-term vision without financial stress.

- Supports Cap Table Optimization: Startups can use secondary sales to clean up the cap table—removing inactive stakeholders and making room for more strategic investors.

- Facilitates Internal Alignment: Giving early team members a chance to cash out creates a fairer ecosystem, improves morale, and aligns incentives across the organization.

Who Generally Sells in Secondary Sales?

In secondary sales, the sellers are typically current shareholders in the startup who wish to partially or entirely exit their equity ahead of a formal exit such as an IPO or acquisition.Such persons or organizations might desire liquidity for personal, strategic, or financial purposes.

The following is an explanation of who generally sells:

1. Founders

- Founders of startups typically sell a portion of their equity in subsequent rounds of funding (typically Series B or later) in order to draw on personal liquidity without leaving the company.

Why they sell:

- To diversify personal financial risk

- To cover personal expenses (housing, taxes, etc.)

- As part of a board-approved structured liquidity program

2. Early Employees

- Members of the team who were granted stock options or equity in the early days of the company can sell shares after the company has appreciated in value and secondary sales are permitted.

Why they sell:

- To capture the value of stock options

- To become liquid after vesting for several years

- Frequently enabled through an employee liquidity program (ELP)

3. Angel Investors & Early-Stage VCs

- Early investors sell all or portions of their interests to late-stage investors to realize gains and balance out their portfolios.

Why they sell:

- To de-risk or exit mature investments

- To release capital to invest in new startups

- When the startup attains later funding rounds or pre-exit stage

4. Former Employees or Departing Executives

- People who are no longer actively engaged with the startup can sell their equity to liquidate it into cash, particularly if they've vested their shares completely.

Why they sell:

- No longer interested in the company

- Want liquidity after leaving

- Need to exercise options within a specified time

5. Secondary Funds & Syndicates (Resellers)

- Occasionally, funds that bought secondary shares themselves may resell the same shares to other investors, particularly in competitive late-stage rounds.

Who Typically Purchases in Secondary Sales?

In secondary sales, the buyers are investors who desire to purchase equity in a startup without affecting current shareholders or issuing new shares.

They prefer to buy late-stage, high-growth, or near-exit startups (such as an IPO or acquisition).

Here is a list of the most typical buyers:

1. Late-Stage Venture Capital (VC) Firms

- These companies invest in later-stage growth startups (typically Series C or higher) and frequently utilize secondary sales to acquire or enhance position without awaiting a new round of financing.

Why they buy:

- Secure access to high-potential startups with established traction

- Accumulate ownership prior to exit

- Prevent dilution by fresh primary rounds

2. Private Equity (PE) Firms

- PE companies tend to make entry through secondary deals when startups achieve notable size or profitability, particularly in industries such as SaaS, fintech, or healthtech.

Why they buy:

- Seeking established startups with stable cash flows

- Strategic acquisition to position themselves for IPO or takeover

- Lower risk than early-stage investment

3. Hedge Funds & Cross-Over Investors

- These investors, such as Tiger Global or Coatue, primarily invest in both private and public firms. They employ secondary buys to gain access to rapidly growing startups before IPOs.

Why they buy:

- Position themselves ahead of public listing

- Take advantage of pre-IPO valuation appreciation

- Diversify through private/public market

4. Strategic Investors or Corporations

- Large technology firms or sector players will acquire shares through secondary sales to engage with relationships or get exposure to disrupting startups without obtaining a full stake.

Why they buy:

- Strategic positioning or pre-partnership

- Potential acquisition pipeline

- Access to innovation at zero R&D cost

5. Existing Investors

- Existing VCs or large shareholders can purchase additional equity in secondary rounds to consolidate their holdings or close out new investors.

Why they buy:

- Double down winners

- Preserve or expand influence and board control

- Unload ownership by less active shareholders

6. Secondary Market Funds

- Specialized vehicles such as Forge, EquityZen, or SharesPost buy secondary shares and resell them to qualified investors in secondary marketplaces.

Why they buy:

- Interested in liquidity in private markets

- Make money from private equity resale at a markup

- Provide access for those who want pre-IPO shares

Why Do Secondary Sales Occur?

Secondary sales occur when existing owners—e.g., founders, employees, or early-stage investors—choose to sell their stake to new or current investors.

These sales are important in the startup world, particularly as firms remain private for longer periods and conventional liquidity events (such as IPOs or acquisitions) are postponed.

Below are the main reasons why secondary sales happen:

1. To Give Liquidity to Founders and Employees

- Startups may take anywhere from 7–10 years or more to attain an exit.

- Secondary sales provide early investors with an opportunity to cash out some of their equity prior to an IPO or acquisition, enabling them to realize some economic value without holding out for a complete exit.

- As per Carta, 70% of late-stage startups provide structured liquidity programs for employees and founders via secondary sales.

2. In order to Facilitate Early Investors to Exit or De-Risk

- Angel investors or seed-stage VCs can sell some or all of their holdings in subsequent rounds to crystallize returns or redeploy capital into new companies.

- This is particularly prevalent after a startup ceases being risky and valuations increase.

3. To Attract New Investors Without Dilution

- Startups can employ secondary sales to attract strategic or late-stage investors without issuing new shares, preventing dilution of existing shareholders or better managing the cap table of the company.

4. To Manage Employee Stock Option Liquidity

- Startups provide equity as part of employee compensation.

- Once a company gets mature, employees can be permitted to sell vested shares through structured liquidity programs in order to incentivize retention and sustain morale.

5. To Rebalance Cap Tables

- Secondary sales can facilitate redistribution of ownership, thin out the pool of dormant shareholders (such as past employees), or consolidate holdings by strategic stakeholders

6. For Preparing for Exit or Entering the Public Market

- Pre-IPOs or large acquisitions, secondary sales tend to happen to tidy up ownership stakes, bring in institutional investors, or address investor demand for pre-exit exposure.

Secondary Sales Considerations and Risks of Startup Funding

While secondary sales provide liquidity and strategic optionality, they also pose significant risks and considerations for sellers and buyers.

It is vital to understand these considerations in order to make reasonable decisions and preserve long-term equity value.

- Signal Risk : Founders or major team members with large or premature secondary sales may send the message that there is a loss of confidence regarding the future of the company, potentially disturbing other employees, investors, or customers.

- Valuation Pressure: Secondary shares sold at lower or higher valuations could influence future capital raises, result in cap table imbalance, or create disagreements during future rounds of investment.

- Dilution Management Complexity: While secondary sales do not dilute the firm directly, they can influence control and ownership structures—particularly if significant blocks transfer hands without board strategy concurrence.

- Limited Buyer Pool: Secondary shares in private startups are illiquid and normally limited to accredited or institutional buyers. Sellers might find it difficult to identify qualified buyers at the appropriate price.

- Legal and Contractual Restrictions: Shareholder agreements typically have Right of First Refusal (ROFR), lock-in periods, and board approval mandates, which can complicate or hinder the sale.

- Tax Consequences: Sellers could be subject to capital gains, and employee option holders might have AMT liabilities, depending on the jurisdiction and timing.

- Misaligned Expectations: Late-entry buyers through secondary shares could anticipate quicker exits, more control, or special privileges—resulting in misalignment with existing founders or investors.

- Effect on Team Morale: When a very limited number of stakeholders enjoy secondary liquidity, it can lead to internal discomfort or dissatisfaction, particularly if others are still stuck.

When to Consider Secondary Sales

1. After Product-Market Fit (PMF)

- When your startup has proven its solution with high demand from customers, recurring revenue, and a reproducible sales model, it's time to think about secondary sales.

- The buyer's risk is lower at this point, and early stakeholders can start releasing some liquidity.

2. While in a Major Funding Round

- Secondary sales usually go hand in hand with major institutional funding rounds (usually Series B or higher).

- These rounds appeal to investors with deeper pockets who are willing to purchase shares from original shareholders to get a toehold in the company.

3. To Retain and Reward Early Employees

- If your early staff possess vested stock options but are low on cash, secondary sales enable them to realize value.

- It's particularly valuable after years of struggle when IPO or acquisition is several years away.

4. When Founders Need Personal Liquidity

- Founders can sometimes get to the point that personal financial pressure impacts performance.

- A modest secondary sale (without losing control) can relieve this pressure and enable them to concentrate on business growth.

5. Investor Rotation or Clean-Up

- Early angel investors, seed funds, or micro-VCs might prefer to exit and recycle capital.

- Permissive secondary sales provide an exit mechanism, clearing the way for new investors with more strategic insights or long-term perspectives.

6. Prior to a Strategic Exit (IPO or Acquisition)

- If an exit event is 1–3 years off, it might be strategic to provide secondary liquidity—particularly to those who will not remain with the company after the exit.

- It also sends a good signal of value creation.

7. Cap Table Management

- If the cap table is cluttered with inactive investors or minor shareholders, a secondary sale can simplify ownership, making future rounds or exits smoother and more attractive to big institutional players.

8. When There’s Strong Market Interest

- Sometimes external demand triggers a secondary sale.

- If investors are proactively requesting to buy shares—even if you’re not raising—this could be an opportunity to bring in strategic partners and offer liquidity.

Structuring a Smart Secondary Sale

- Time It Right: Do secondary sales after key milestones like a major funding round or strong revenue growth—it boosts credibility and valuation.

- Define Clear Goals: Know why you’re doing it—founder liquidity, early employee rewards, or investor rotation. Keep the purpose aligned with long-term growth.

- Control Who Sells and How Much: Limit sales to early stakeholders and cap individual sales (e.g., 10–20% of holdings) to maintain cap table stability.

- Set Fair Pricing: Base pricing on recent primary valuation. Avoid overpricing or deep discounts—both can damage your perception.

- Ensure Legal Compliance: Use formal transfer agreements, update your cap table, get board approval, and follow securities regulations.

- Vet Buyers Carefully: Choose buyers who are strategically aligned, not just transactional. Reputation and intent matter.

- Communicate Transparently: Keep your board, lead investors, and legal team informed. Transparency builds trust.

- Avoid Negative Signals: Too much insider selling can signal doubt. Keep it modest and well-timed.

- Make It Part of a Bigger Plan: Integrate the sale into a long-term liquidity strategy—don't treat it as a one-off payday.

Secondary Sales vs. Primary Rounds vs. IPO

- All secondary sales, primary rounds, and IPOs are liquidity events in startup funding—but they are used for different reasons and parties.

- Secondary sales mean current shareholders (such as founders or early staff) selling their equity to new or existing investors.

- None of the company sees new capital, but it provides investor turnover and personal liquidity.

- On the other side, early-stage funding rounds (such as Seed, Series A, B, etc.) add new capital to the startup for newly issued stock, driving business growth, hiring, R&D, or expansion into new markets.

- And then there's the IPO (Initial Public Offering)—the most visible and risky path—where a private startup goes public on a stock exchange and issues stock to the public.

- IPOs are big money raisers and provide complete liquidity but with regulatory costs and market pressures.

- Every path has its time and place in a startup's lifecycle—and recognizing the differences is essential to handling growth, dilution, and strategic exits judiciously.

Final Thoughts: Secondary Sales Are a Strategic Power Move

Secondary sales aren’t just about early cash-outs—they’re a calculated move to align incentives, retain top talent, and bring in fresh strategic investors.

When timed right, they offer founders and early backers well-earned liquidity without slowing down the company’s momentum.

As startups delay IPOs and large acquisitions, secondary transactions offer a flexible middle path—bridging personal financial goals with the startup’s long-term vision.

For fast-growing startups, they can de-risk founders’ journey, reward early believers, and clear the cap table for future growth.

"Smart startups don’t wait for the finish line—secondary sales let them win while they build.